Important notice

The comments below are provided for general informational purposes only. They are intended as broad market observations based on industry experience and do not constitute financial product advice, legal advice, or a recommendation in relation to any particular insurer, policy, or insurance structure.

Insurance decisions should be made only after considering the specific circumstances of the insured, the policy terms, applicable regulations, and appropriate professional advice where required.

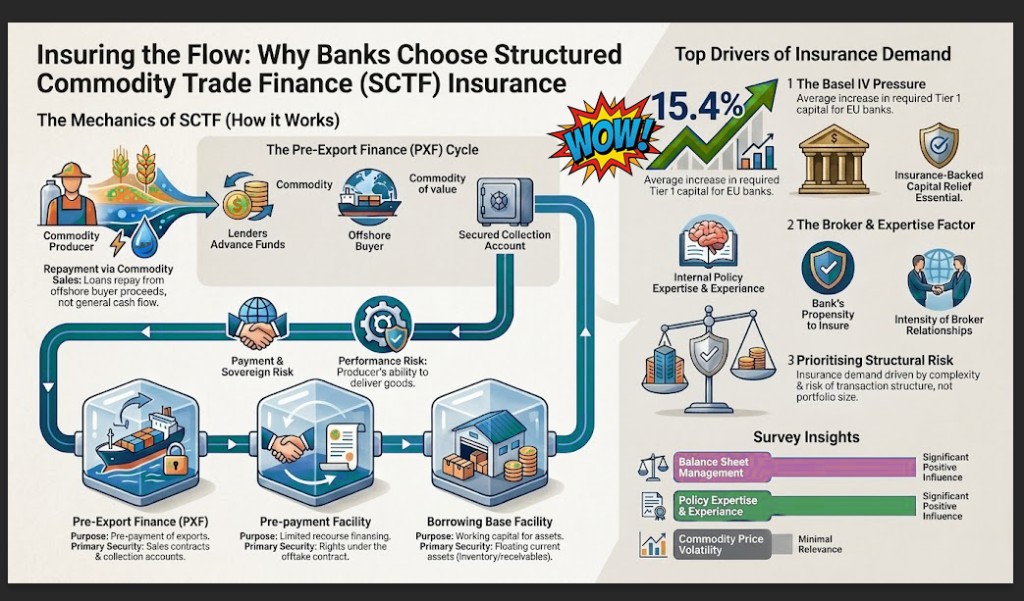

Pre-export finance arises when a commodity producer needs funding before goods are produced and exported. Rather than relying only on the producer’s balance sheet, the bank lends against future commodity sales. Repayment is then directed through offshore buyer payments and controlled collection accounts. This structure helps banks reduce direct borrower exposure while managing payment, sovereign, and producer performance risk.

Structured Commodity Trade Finance commonly appears in three forms: Pre-Export Finance, where producers receive funding before export; Pre-payment Facilities, where a trader or buyer advances payment linked to an offtake contract; and Borrowing Base Facilities, where working capital is secured against inventory, receivables, and other current assets.

Specialty Credit Insurance fits SCTF because these transactions are bespoke, cross-border, and often exposed to emerging-market risks. Unlike standard short-term trade credit insurance, it can be tailored to complex structures, cover both commercial non-payment and political or sovereign risks, and support banks seeking capital relief, exposure management, and protection against structural transaction risk.

The survey shows that banks’ demand for SCTF insurance is mainly driven by balance sheet management, product expertise, structural transaction risk, and broker relationships. Basel III and Basel IV have made SCTF exposures more capital intensive, so banks increasingly use insurance not only for risk transfer, but also to reduce risk-weighted assets, improve leverage ratios, and achieve regulatory capital relief.

The survey also suggests that knowledgeable and well-connected brokers have contributed to the growing adoption of SCTF insurance. Because SCTF insurance is niche and technically complex, brokers help banks understand the product, structure bespoke solutions, negotiate policy wording, advise on capital treatment, and connect banks with specialist insurers. In this sense, broker expertise has helped increase both familiarity with and demand for the product.

The key message is that SCTF insurance has evolved from a simple credit protection tool into a strategic balance sheet and risk-management solution for banks involved in complex cross-border commodity finance.

Unsure whether your current credit insurance structure is appropriate? Zenith Credit-Solutions can provide an independent review of policy structure, insurer selection, and market options.

Disclaimer

This material is general in nature and is not intended to influence any person in choosing, acquiring, varying, or retaining a specific financial product. It does not take into account any person’s objectives, financial situation, or needs. Readers should obtain appropriate professional advice before making any insurance or risk management decision.