Independent trade credit insurance advisory with a global perspective, helping businesses strengthen structures, broaden market access, and secure better outcomes through practical specialist insight.

Our mission was formed in response to a clear gap in the Australian market.

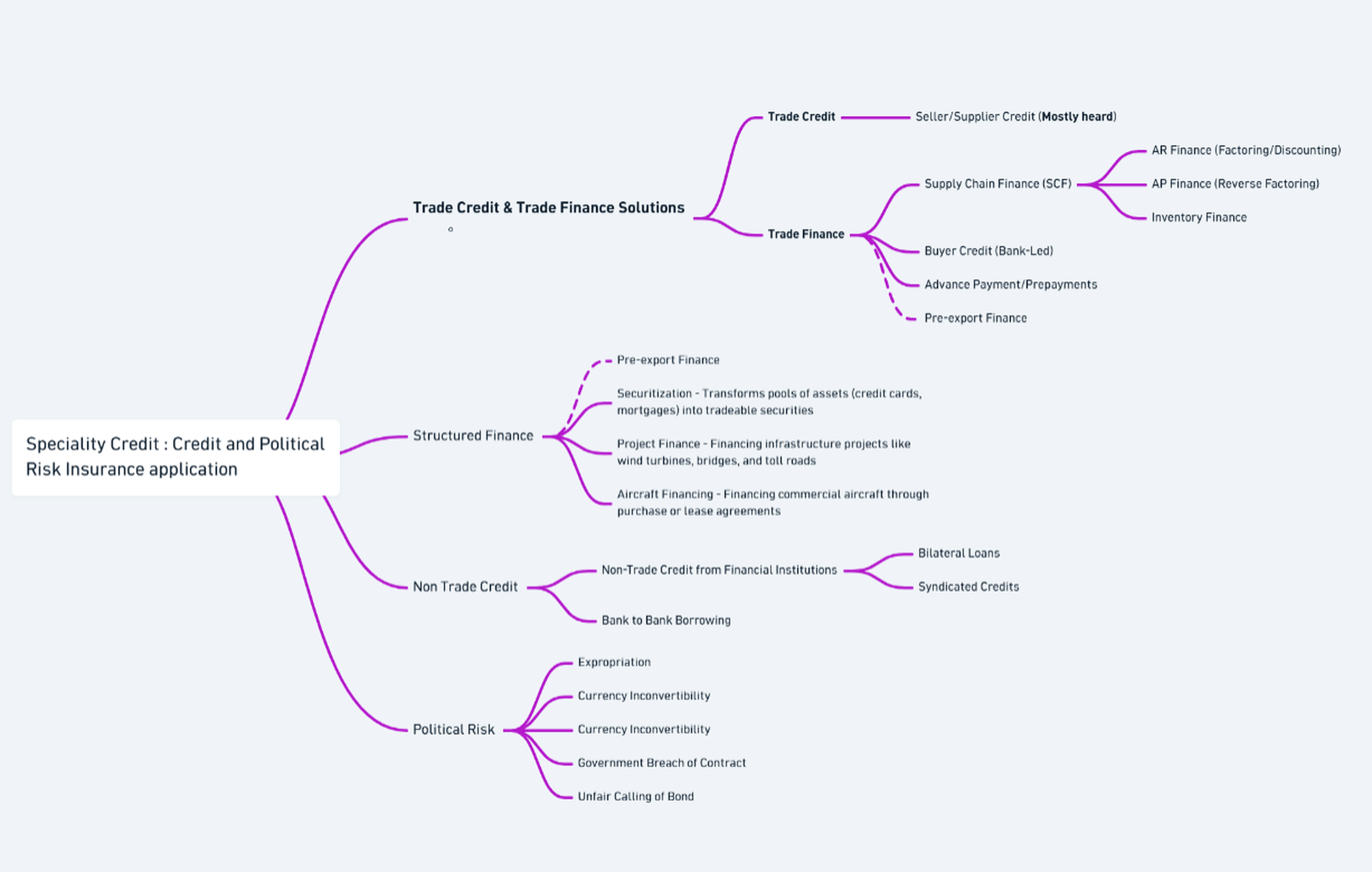

Trade credit insurance in Australia remains shaped by a relatively limited pool of insurers, with solutions often concentrated around traditional whole-of-turnover portfolio structures. In many cases, client needs are not fully served — whether in terms of required limits, product variety, or flexibility of structure. Yet internationally, the use of credit insurance has evolved well beyond its conventional role in trade finance. In more developed markets, it is increasingly used across broader financing and non-trade contexts, including financial institution lending and other structured applications. The following diagram illustrates how the scope of Specialty Credit and Political Risk insurance extends significantly beyond standard, short-term whole-of-turnover trade non-payment policies. While this overview captures the core pillars of the broader international market, it is by no means exhaustive; many specialized global insurers design highly customized facilities that push these boundaries even further.

Even within the trade finance space, the Australian market continues to lag behind international practice. Policy terms, structures, and negotiation outcomes can often be far more flexible than many buyers realise, provided the client has the knowledge and leverage to engage the market effectively.

With solid experience across both local and overseas markets, our aim is to help bring a new perspective to this sector — one grounded in education, practical insight, and commercial independence. We believe credit insurance should be understood not only as a protection product, but as a broader financial management tool: one that can strengthen credit discipline, support better receivables management, and in some cases enhance financing outcomes with banks.

For many businesses, credit insurance appears complex and difficult to access. Our view is that a significant proportion of cases can be handled more directly by the business itself when supported by the right knowledge and industry understanding. The benefit is not only the reduction of recurring brokerage costs, but also the ability to negotiate more effectively with insurers and extract greater value from the policy itself.

At its core, our mission is to educate the market, widen access to better solutions, and help clients use credit insurance in a more informed, cost-effective, and strategically valuable way.

We help clients use insurance more strategically — with greater independence, sharper structuring, and access to broader market capability where local solutions fall short.

In Australia, the credit insurance market remains relatively concentrated, with only a handful of insurers actively participating in this space. As a result, many buyers are channelled through a narrow distribution structure, where the default outcome is often the purchase of insurance rather than a broader assessment of whether the cover is necessary, efficient, or properly structured. For clients with relatively straightforward insurance needs, it is entirely feasible to take greater control of the process with the right specialist guidance. This can lead to significant savings by avoiding recurring brokerage costs and by ensuring that insurance is only used where it genuinely adds value. Our approach starts from a different premise. Rather than assuming more insurance is the answer, we examine your portfolio from a risk management perspective — identifying where protection is truly needed, where premium spend may be unnecessary, and how insurance can be used more selectively and effectively. The objective is not simply to buy a policy, but to maximise meaningful protection without paying for cover that does not materially improve your risk position.

We combine market understanding, practical judgement, and creative thinking to help clients navigate a specialist market where access, structure, and credibility matter.

We bring more than technical product knowledge. We bring a deep understanding of how this specialist market truly works — including the relationships, market dynamics, and international networks that often determine whether a transaction can be achieved on the right terms.

In credit and political risk insurance, access and credibility matter. Our knowledge extends beyond policy mechanics to the practical realities of negotiating with insurers across different markets.

Our advice is grounded in real market experience across both the private and public sectors, covering underwriting and, critically, claims.

This matters because many market participants may understand placement, but far fewer understand how insurers assess risk internally or how a policy is likely to respond when tested by a claim. It gives our clients practical insight that is commercially relevant from the outset.

The market is evolving quickly. Where conventional markets fall short, we help clients explore novel solutions. This may involve identifying emerging insurers, new structures, or alternative approaches that better reflect current market realities.

For more complex transactions, the ability to think beyond standard solutions can be the difference between a declined opportunity and a workable outcome.

Our work is informed by international market awareness, disciplined analysis, and an appreciation of how credibility, structure, and perspective shape better outcomes.

Our advice is supported by more than 30 years of combined credit-sector experience, including specialist credit insurance exposure across private and public sector markets in Australia, Asia-Pacific, and the UK.

Clive Mok CPA, BCom, BSc, MA

Email: c.mok@zenithcreditsolution.works

As a qualified CPA, Clive began his career with broad-based training across both claims and underwriting in trade credit insurance, building a practical understanding of risk from policy structuring through to claims outcomes. Since then, he has worked with several leading credit insurers across both public and private sectors, holding various roles throughout the Asia-Pacific region.

Over time, his focus expanded into structured credit and political risk insurance, where he has been involved in developing new markets and supporting more specialised financing transactions across the region. This includes experience across trade finance, receivables finance, supply chain finance, project finance, and political risk solutions, working alongside banks, brokers, insurers, and export credit agencies across multiple jurisdictions.

Clive is multilingual and experienced in cross-cultural environments, with an ability to navigate commercial and structural issues across different markets and identify the broader context behind complex transactions. He takes a practical and thoughtful approach to risk, balancing technical detail with commercial outcomes.

Beyond his longstanding interest in geopolitics and international markets, Clive has a strong interest in how artificial intelligence can be applied within underwriting and credit analysis. He believes emerging technology has the potential to improve transparency, reduce unnecessary process friction, and support more efficient outcomes for both insurers and clients—while keeping commercial judgement and human insight at the centre of decision-making.

We welcome enquiries from businesses, brokers, and financial institutions seeking clearer guidance on credit, trade, and political risk insurance. While our principal focus is the Australian market, we also welcome discussions involving Hong Kong, Singapore, Taiwan, and the broader Asia-Pacific region. Support is available in English, Cantonese, and Mandarin.

Have a question, comment, or matter you would like to discuss? Please feel free to get in touch.